This is the most common question we get asked. Whether it’s a conversation at a wedding, during a meeting, or talking to mates in the pub. “How much do I need? How much should I have? I have £100,000 – is that enough?”

It doesn’t matter how it’s worded, everyone is looking one of two things – either to have something to aim for or to compare themselves against others. It’s human nature to want both of these things, so don’t feel bad admitting it. It seems like a simple question, but the answer is far from it.

What Kind of Lifestyle Do You Want?

We will always answer with a variation of “It depends….” But what we are really asking is “what do you want your retirement lifestyle to look like?”

- Are you used to holidays abroad?

- Would you only buy new or nearly new cars?

- Are you happy to buy wine from the supermarket or does it need to come from a wine club?

- Are you a Lidl or an M&S regular? (we love a bit of Lidl here)

As you can see the answer is always going to be different for everyone.

Luckily for us, the UK government did some research to put some figures towards this. Let me introduce you to the Pensions and Lifetime Savings Association (PLSA) Retirement Living Standards study. This study was completed in October 2019 so figures will be higher now (due to inflation) and is a UK average.

The study’s aim was to show how much of an annual income you may need each year. It depends on whether you are single or in a couple, and whether you want a Minimum, Moderate or Comfortable lifestyle.

| Single Person | A Couple | |

| Minimum Lifestyle | £10,200 per year | £15,700 per year |

| Moderate Lifestyle | £20,200 per year | £29,100 per year |

| Luxury Lifestyle | £33,000 per year | £47,500 per year |

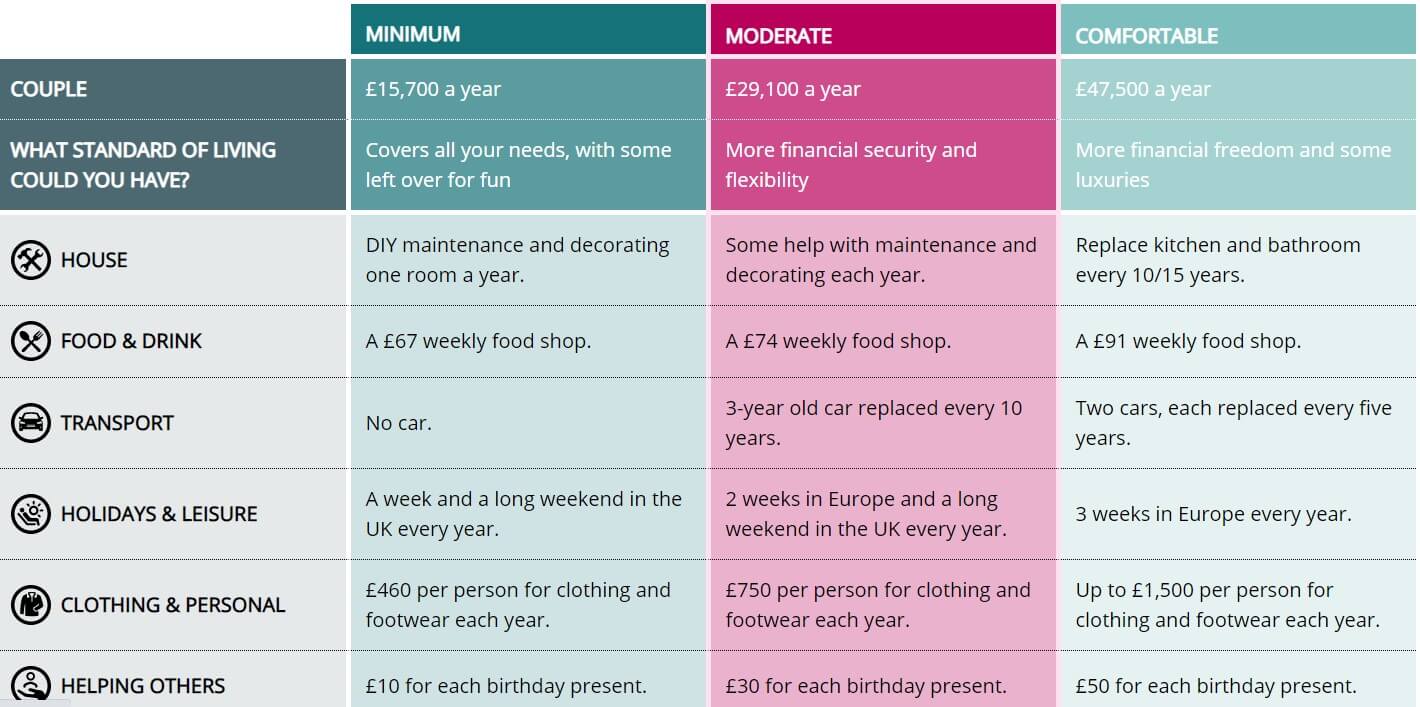

To put some context to what each of these lifestyles looks like, they have produced this infographic. This is for a couple:

If you are interested in finding out more, go to https://www.retirementlivingstandards.org.uk/ for full details of their research.

I Know What I Need

You can only start planning when you have an idea of what your lifestyle will look like, or rather, what you want it to look like. Remember a full current state pension pays £179.60 per week (in tax year 2021-22), which for 52 weeks gives an annual income of £9,339.20. So, a full state pension does not provide sufficient income for a single person to live the minimum standard of living, according to the above research. However, for a couple, with two full state pensions, they would have a combined income of £18,678.40 which does cover the minimum lifestyle for a couple.

Have you other savings or investments which will help to contribute towards this?

- Maybe you have several pensions? (There are 2 types of pension

- Defined contribution pension – there is an actual fund / pot of money

- Defined benefit pension – you have a guaranteed income for life.

- Perhaps you have rental properties, or you’re planning to downsize.

- Do you have a business to sell?

- Or are you expecting a big inheritance?

There is so much which can come from the question of “How much do I need?”

The thing about the State Pension is that you have no control over when you will receive the benefits (currently age 66, 67 or 68)! So if you want to retire aged 55 then you will need other forms of income to help you live your desired lifestyle.

Can I afford it?

As a very simple rule of thumb, your pension fund value should safely provide you with an income of 4% per annum. So if you have £100,000 in your pension, you should be able to withdraw £4,000 per annum (increasing with inflation each year) and not run out for 30 years.

You might already know what your income will be in retirement. Or, you have lots of “stuff” and no idea how it all comes together. That’s when you need to start doing something about it.

Here are 3 action points to help you begin your retirement review –

- Check your state pension forecast. If you have never done it, it’s really straightforward to do it yourself online – https://www.gov.uk/check-state-pension

- Gather your documents up! If you have a mix of savings, pensions, property and investments, it is probably worth speaking to an independent financial planner (like us) who will help you make more sense of it all.

- Research! If you aren’t quite ready to speak to someone, but you want to know more, then sign up for our free webinar on Thursday 14th October. We will cover in more detail what you need to think about when it comes to planning for your retirement lifestyle. We will be using the example of what £500,000 could provide for your retirement lifestyle.

By using the very simple rule of thumb that your income is 4% of the fund, £500,000 would then provide an annual income of £20,000 per annum. To put that in context, for a single person, that provides a moderate lifestyle. However, if it’s split between a couple, you are £10,000 per annum short of a moderate lifestyle.

Would you be happy to settle for a retirement with no car, holidays within the UK and spending just £67 per week on food and drink? If not, now is the time to do something about it.